24 January 2022

- The technical standards aim to ensure that stakeholders are well-informed about institutions’ ESG exposures, risks, and strategies and can make informed decisions and exercise market discipline.

- The standards put forward comparable disclosures and KPIs, including a green asset ratio (GAR) and a banking book taxonomy alignment ratio (BTAR), as a tool to show how institutions are embedding sustainability considerations in their risk management, business models and strategy and their pathway towards the Paris agreement goals.

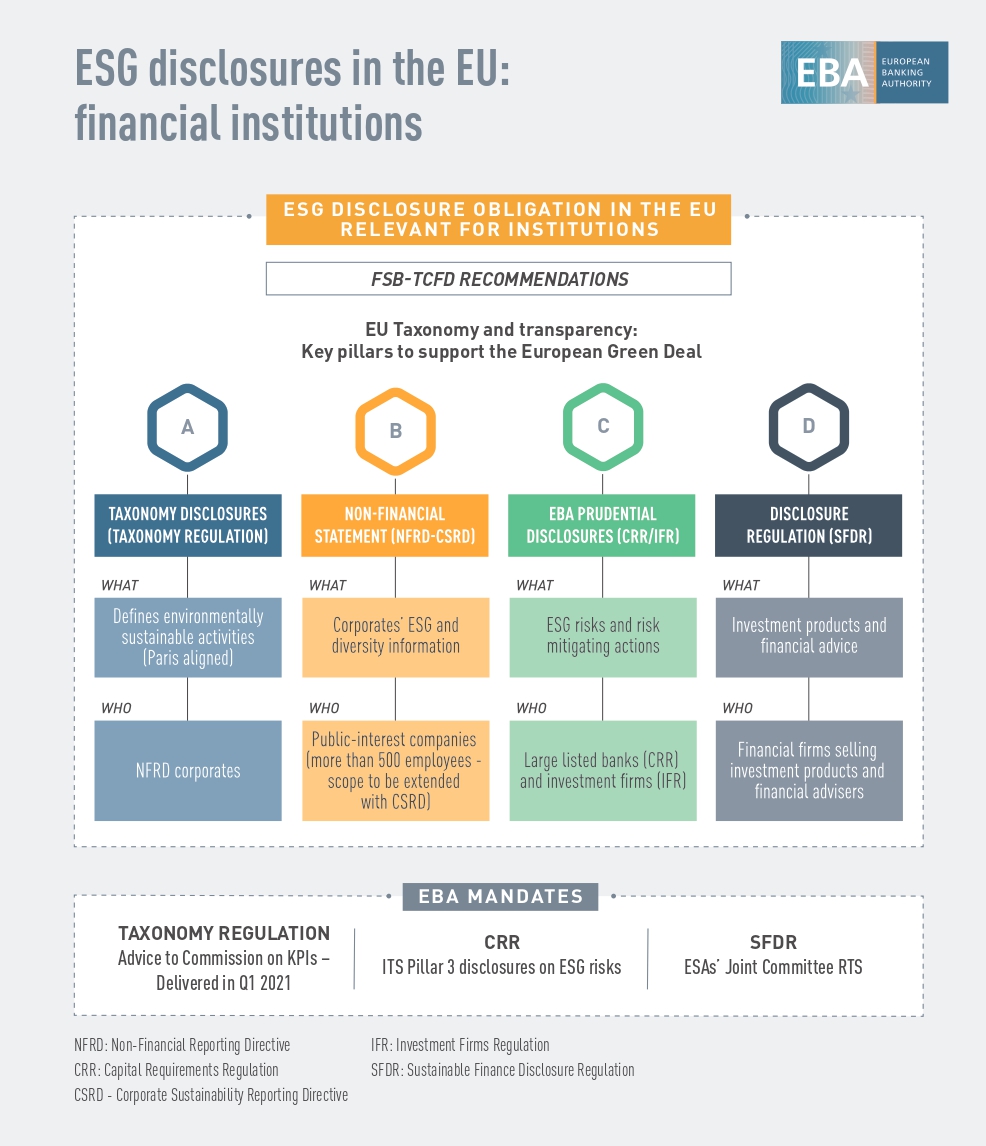

- In developing this framework, the EBA has built on the recommendations of existing initiatives, like those of the Task Force on Climate-related Financial Disclosures (TCFD) of the Financial Stability Board (FSB), but has gone beyond by defining binding granular templates, tables and instructions, to ensure enhanced consistency, comparability and meaningfulness of institutions’ disclosures.

The European Banking Authority (EBA) published today its final draft implementing technical standards (ITS) on Pillar 3 disclosures on Environmental, Social and Governance (ESG) risks. The final draft ITS put forward comparable disclosures to show how climate change may exacerbate other risks within institutions’ balance sheets, how institutions are mitigating those risks, and their ratios, including the GAR, on exposures financing taxonomy-aligned activities, such as those consistent with the Paris agreement goals.

Disclosure of information on ESG risks is a vital tool to promote market discipline, allowing stakeholders to assess banks’ ESG related risks and sustainable finance strategy. The EBA ESG Pillar 3 package will help to address shortcomings of institutions’ current ESG disclosures at EU level by setting mandatory and consistent disclosure requirements, including granular templates, tables and associated instructions. It will also help establish best practices at an international level.

In line with the requirements laid down in the Capital Requirements Regulation (CRR), the draft ITS set out comparable quantitative disclosures on climate-change related transition and physical risks, including information on exposures towards carbon related assets and assets subject to chronic and acute climate change events. They also include quantitative disclosures on institutions’ mitigating actions supporting their counterparties in the transition to a carbon neutral economy and in the adaptation to climate change. In addition, they include KPIs on institutions’ assets financing activities that are environmentally sustainable according to the EU taxonomy (GAR and BTAR), such as those consistent with the European Green Deal and the Paris agreement goals.

Finally, the final draft ITS provide qualitative information on how institutions are embedding ESG considerations in their governance, business model, strategy and risk management framework.

The EBA has integrated proportionality measures that should facilitate institutions’ disclosures, including transitional periods and the use of estimates.

Legal basis and background

Article 434a of the Capital Requirements Regulation (CRR) mandates the EBA to develop draft implementing technical standards specifying uniform disclosure formats, and associated instructions in accordance with which the disclosures required in Part eight of the CRR shall be made. Those uniform formats shall convey sufficiently comprehensive and comparable information for users of that information to assess the risk profiles of institutions.

The ITS will amend the final draft ITS on institutions’ public disclosures with the strategic objective of defining a single, comprehensive Pillar 3 framework under the CRR that should integrate all the relevant Pillar 3 disclosure requirements. This will facilitate institutions’ implementation and enhance clarity for users of such information, as expressed in the EBA Pillar 3 roadmap.

When developing these standards, the EBA has built on the Financial Stability Board Task Force on Climate-related Financial Disclosures (FSB-TCFD) recommendations, the Commission’s non-binding guidelines on climate-change reporting, and on the EU Taxonomy.

DOCUMENTS

- Draft ITS on Pillar 3 disclosures on ESG risks

- Annex I - Templates for ESG prudential disclosures (XLSX)

- Annex II - Instructions for ESG prudential disclosures templates

- ESG Pillar 3 disclosures Factsheet (updated)

- ESG disclosures in the EU - financial institutions.jpg

- EBA summary of ESG disclosures - Pillar 3.jpg

{kind=link}

{kind=link}

LINKS